What are pay advances and should you be offering them?

- Feb 15, 2024

- 8 min read

This blog post was originally created for ZayZoon on February 15th, 2024. Find the original post here.

--

Supporting your employees' financial journey

Sometimes, there’s just not enough money to cover all the costs that pile up. This is not a unique story, as we know that 63% of Americans live paycheck to paycheck.

In times like these, employees will often turn to someone they trust. They'll look to you, their employer, to have their back.

As a people leader, you have probably seen this before. Someone is at the end of their rope and needs a break.

That’s where pay advances come in.

Pay advances (or cash advances) are a way for business owners to support their employees. They offer help when employees need a push to stay afloat. They’ve become the norm in many industries. They also help employees avoid predatory loans or defaulting on their bills.

But how do they work and how do you know if it’s the right path for your business?

We surveyed more than 20 business owners to dig deeper into pay advances. We wanted to find out if there’s a better alternative to support your employees in times like these.

Spoiler alert: there is.

An introduction to pay advances

Pay advances are a financial solution designed to bridge the gap between paychecks. They are typically small, short-term loans that provide immediate funds directly into a bank account.

“In certain situations, this mechanism can demonstrate that the company is looking out for their employees beyond the ‘hourly rate’,” says the founder of a medical practice.

Pay advances have become the norm in many industries. It’s no wonder, as 36% of American households have trouble paying off at least one bill or expense.

Source: survey of more than 5,000 ZayZoon customers across multiple industries

What is a pay advance?

A pay advance is a way to borrow money against future earnings. Employees can access their earned wages before their next payday. It’s a popular option, with millions of pay advances issued each year in the U.S. alone.

People typically request a pay advance when faced with unexpected expenses or financial shortfalls during their pay period. They are not meant to replace regular income or to be used for large purchases. They are designed to provide a financial safety net during times of need.

Employee loans vs. pay advances

The terms might be used interchangeably. But employee loans, payday loans, and pay advances are not the same.

Here’s a breakdown of each:

Employee loan: A personal loan from an employer to the employee. It's usually paid back in installments from future paychecks.

Pay advance: An advance on their future earnings which are deducted on payday.

Payday loan: A short-term loan provided by payday lenders with high-interest rates.

All three methods allow an employee to access a part of their paycheck ahead of payday. Only the first two are offered by employers, though. Payday loans are offered by predatory lenders.

They all have inherent risks that need to be taken into account.

Payday loans are the clearest example. These often come with annual percentage rates (APR) of 300-500% or more. This is because of their high-interest rates. This often leads to employees being stuck in a vicious cycle trying to pay them back. In fact, a 2015 study by the Pew Charitable Trusts found that 12 million Americans take out payday loans each year. They spend $7 billion on loan fees.

Employee loans and pay advances can also come with risks. These include a shortfall in the business’s cash flow, risk of non-payment, and more. We’ll dive deeper into these shortly.

Why is offering pay advances important?

Offering employees money might seem counterintuitive. You already pay them a living wage. However, when speaking with business owners, we found that it’s really important to be there for their employees when they need them. It leads to a better work culture. Moreover, it can also increase employee productivity, retention, and engagement.

So, why do business leaders choose to offer pay advances? Here’s what they said:

For some, it’s about being there for their people:

“I think it's important to show your employees that you have their back and will take the time and money to help them through a difficult time. It builds trust and respect in two directions," says the owner of a consumer electronics company.

For others, it’s about allowing their staff to be more engaged and productive at work:

“It’s important to take care of your employees. I want them to feel supported and like we trust them. And I don’t want an emergency to ruin their situation. If someone is really stressed about needing money they’re not going to be able to do well at work,” says the owner of an e-commerce business.

He’s right. In fact, 84% of employees report worrying about their finances at work. This affects their productivity and engagement daily.

Offering pay advances is not a requirement, but many businesses choose to do so. This signals to employees that their financial well-being is a priority. This can boost morale, increase productivity, and even help attract and retain talent.

As an employer, being there for your employees during a financial crunch is invaluable. It fosters loyalty and can improve the overall work environment.

The risks of pay advances

Offering pay advances, however, does come with potential pitfalls. The risk of an employee leaving without repaying the cash advance, for instance, could affect the company’s cash flow.

50% of business owners we surveyed for this piece said they’d had at least one instance where an employee had not paid back their advance. Source: Independent survey of 30 business leaders across multiple industries. February 2024.

Moreover, the fees for administering pay advances can add to the company’s workload and costs. It requires careful tracking and additional payment processing. This can be a burden, especially for small businesses.

This was the case for Gray America Corp, a leading global manufacturer of steel products. They prioritized supporting their employees in times of need. Nonetheless, this meant they were processing about 20-plus loans at any given time. Their annual labor hours and banking costs were around $8,000 (or 150 hours) a year. This wasn’t working.

Offering pay advances has other risks. These include not knowing how to run it through your payroll system.

Also, having employees rely on advances constantly; and figuring out how to tax these advances properly.

How to set up a pay advance policy

If you decide to offer pay advances, make sure to implement a policy that clearly outlines expectations and pay period.

Setting up a proper pay advance policy:

Define the purpose and scope of the pay advance policy.

Determine who is eligible for a pay advance.

Specify the maximum amount that can be advanced.

Outline the repayment terms.

Detail the process for requesting a pay advance.

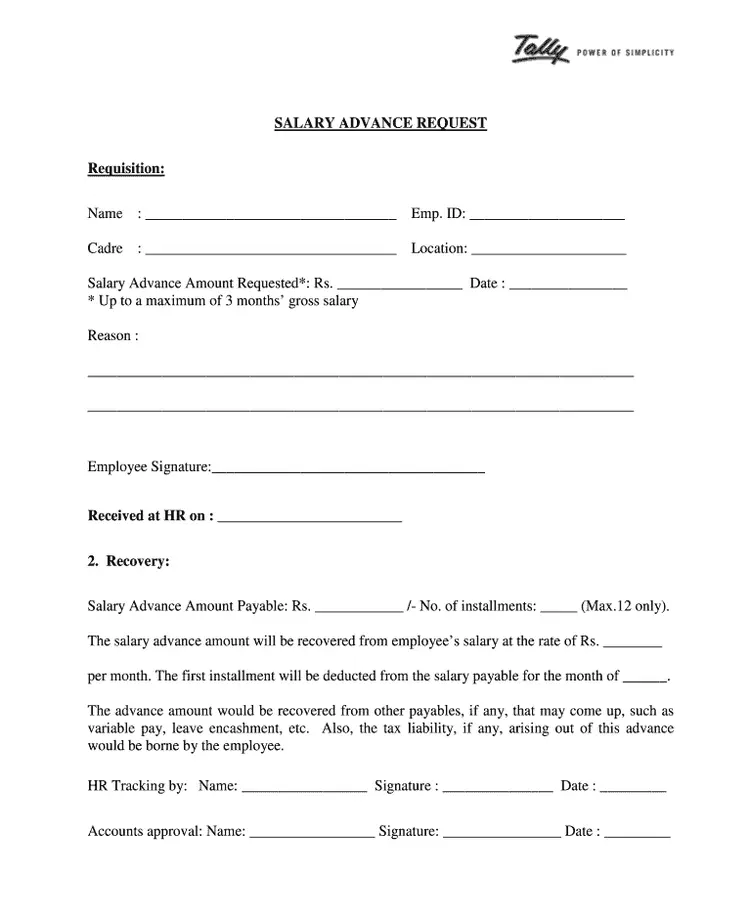

It is essential that you make no exceptions to this policy and ensure that you have every step in writing. For example, a request form could look something like this:

If you’re trying to protect your business while taking care of your employees, a well-structured policy will help navigate potential pitfalls, protect your business, and ensure fair treatment of all employees.

Pay advances for SMBs

The risks and considerations associated with pay advances vary based on the size of the business. Larger enterprises often have more financial capacity. They can absorb the potential risks associated with this practice.

For SMBs, it is crucial to consider the financial capacity of the business to offer pay advances. Establish clear guidelines to manage the risk effectively, including monitoring bank accounts. Consider also having a separate credit limit to manage the ebbs and flows of this offering.

When surveying business owners for this piece, we found a mix of informal and formal procedures for pay advances.

In fact, only 50% of those surveyed had an established process for employees to ask for an advance. All of them were SMBs.Source: Independent survey of 30 business leaders across multiple industries. February 2024.

To ensure the success of your business in the long run, having a proper process and ensuring that everyone follows it can be the deciding factor.

How to run a pay advance through payroll

Running pay advances through payroll may seem complicated. Yet, it is a practical process. Once established, it should be easy to replicate. Once the advance is approved, the cash amount can be processed as a regular payroll run. It can be disbursed to the employee’s bank account via direct deposit.

One thing to bear in mind is that pay advances might be taxable. Therefore, it’s crucial to consult with a tax expert or payroll software provider. This is to ensure compliance and accurate tax reporting.

Should you offer pay advances?

As with many business choices, pay advances can be a tricky one to navigate. Pay advances can provide a lifeline for employees in financial distress. However, they might also encourage dependency and lead to long-term financial instability.

Moreover, there’s a risk of financial loss for the company if employees fail to repay the cash advances made. This, coupled with the added administrative workload and complex regulatory landscape, makes the decision to offer pay advances a significant one.

Are pay advances right for your business?

To determine if pay advances are suitable for your business, you’ll need to weigh various factors. Consider the financial implications, your capacity to manage the program, and the legal and regulatory requirements.

Remember, offering pay advances should align with your company’s financial objectives and policies. It’s important to have safeguards in place to prevent abuse of the program.

Earned Wage Access:

The reality is that employees don’t like asking for a cash advance but sometimes they don’t have a choice.

Employers often can’t offer this option because they consider the risks, administrative burden, and their capacity to customize payroll runs. No matter how much they want to support their employees.

Which is where Earned Wage Access (EWA) comes in. With Earned Wage Access, employees get their wages when they need them and you don’t need to lift a finger.

EWA provides employees with immediate access to their earnings. It also eliminates the risk for employers. Businesses can offer this benefit without straining their resources or cash flow by partnering with a third-party EWA provider.

The benefits to your business go beyond doing the right thing for your people. Some of these include:

Low lift: EWA is a plug-and-play solution, with setup being as short as 30 minutes

Low risk: EWA providers take on the risk themselves, protecting your business

No maintenance: customer support is handled by the EWA support team

Integration with payroll: EWA providers integrate with your payroll system, so you don’t need to manage the advances

Zero cost: Offering EWA costs you nothing

Businesses that offer ZayZoon Earned Wage Access have shown a 29% reduction in turnover. And they get 2X more applicants than they did before offering EWA.

Remember how I said there was a better alternative to pay advances? This is it.

Looking forward

It’s no secret that financial wellness is essential. It's key to being competitive and retaining the best talent. Thankfully, employee benefits like EWA make it possible for you to offer all the benefits of pay advances. You can do this without the hassle and risk associated with this antiquated benefit.

Whether you offer pay advances, implement an EWA program, or find other ways to support your employees financially, remember that the ultimate goal is to foster a supportive work environment. It should value your employees’ financial well-being and help them continue to grow.

You’ve got this.

Comments